Tiếng Việt

Tiếng Việt

Freight indexes have become divorced from the reality of the market according to consultant Jon Monroe, who says that no index accurately represents the rate a shipper needs to pay to ship a container to the US.

Ship operator profits increased from the middle of 2020 and have continued to grow into this year, with Yang Ming and HMM the latest lines to declare first quarter profits, and in HMM’s case, they represent historically high returns.

“Today’s environment is a free for all and it seems carriers are looking to get what they can, while they can,” claimed Monroe, who asked “where is this coming from? Out of our pockets of course,” he said answering his own question.

According to Monroe’s contacts the freight indexes are broken, they have rates of around US$5,600/FEU from China base ports to the US West Coast and US$7,450/FEU tot eh East Coast. While rates the lines have published to NVOCC’s are around US$4,300/FEU and US$5,600/FEU respectively.

A small percentage of shippers may be able to achieve rates of US$6,500/FEU, more likely the cost will be far higher. “I see rates quoted from the carriers at US$9,000 and higher. Zim for example, has quoted as much as US$14,000 to Oakland and Evergreen as much as US$17,000 from China base ports to East Coast. Zim Lines also increased their premium from US$3,000 to US$5,000 last month. Few companies can get containers onboard vessels at published FAK rates,” said Monroe.

These rates appear to have become the norm as demand for space, far from diminishing from last year’s highs, continues to soar to ever higher heights. The National Retail Federation (NRF) has said it expects 2021 to be a record year for demand as the economy reopens following the pandemic.

This is in part good news, however, the lack of equipment and capacity, including chassis, containers and inland rail transportation has led Monroe to warn that shippers are faced with the prospect of only getting a fraction of their cargo on board ships and advises that cargo shipments should be booked four to six weeks in advance in an effort to get the freight to market on time.

“There is no plan B for this situation. Right now, relationships are more important than ever. Stick with your current carrier and NVOCC, ensure your communications are transparent and move what you can,” added Monroe.

All the pointers currently show that the situation in the US will continue into 2022 with shortages of containers, a lack of vessel capacity, congested ports and disrupted inland services either by truck or rail.

According to Monroe, “In summary what is the correct rate? The correct rate is one that gets a container onboard a vessel. That rate is whatever the carrier will accept to prioritise the container to be loaded on board a vessel. I do not think this rate is included in any of the indexes.”

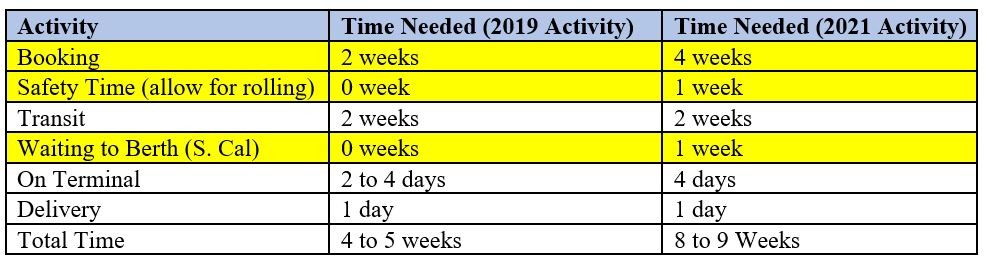

The chart below reflects the new normal for lead time. Add four to five weeks to your current order cycle for west coast delivery and another one to two weeks for inland transportation.